IFRS 9 is the International Financial Reporting Standard that addresses accounting for financial instruments. It includes guidance on expected credit loss (ECL) modeling, also known as the impairment of financial assets.

Here are the key principles of the expected credit loss model as per IFRS 9:

- Classification of Financial Assets: IFRS 9 requires financial assets to be classified into one of three categories: Amortized Cost, Fair Value through Other Comprehensive Income (FVOCI), or Fair Value through Profit and Loss (FVPL). The classification depends on the business model for managing the financial assets and their contractual cash flow characteristics.

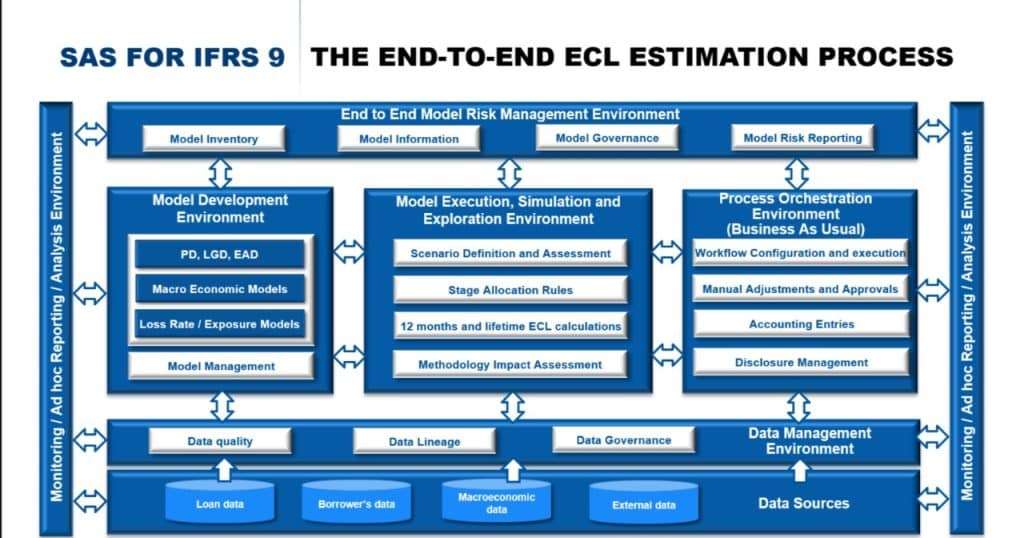

- Impairment Model: IFRS 9 introduced a forward-looking ECL model to determine impairment for financial assets. This model is more proactive in recognizing credit losses compared to the previous “incurred loss” model under IAS 39.

- Three Stages of ECL: The ECL model in IFRS 9 has three stages for measuring expected credit losses:

a. Stage 1: At initial recognition of a financial instrument, ECL is measured based on the probability of default in the next 12 months.

b. Stage 2: If there is a significant increase in credit risk since initial recognition but the financial instrument has not yet experienced a credit loss event, ECL is measured based on the lifetime expected credit losses.

c. Stage 3: When a financial instrument is considered credit-impaired, ECL is measured based on the lifetime expected credit losses.

- Measurement of ECL: The measurement of ECL requires an entity to consider a range of information, including historical credit loss experience, forward-looking information, and reasonable and supportable economic assumptions. It involves estimating the probability of default, the exposure at default, and the recovery rate.

- Regular Updates: Entities are required to regularly update their ECL calculations to reflect changes in credit risk. This means that financial statements should reflect the most current information available.

- Disclosure: IFRS 9 also mandates extensive disclosures regarding the ECL model, including details about significant judgments and assumptions used in estimating ECL, changes in ECL allowances, and the credit quality of financial assets.

- Hedge Accounting: IFRS 9 also includes provisions for hedge accounting to align it more closely with risk management practices.